Penn Foster 06155200: Graded Project

Lesson 1: Business, Accounting, and You (J&L Accounting, Inc.)PROJECT GOAL

The goal of this graded project is to create the following financial statements for J & L Accounting, Inc.:

– Balance sheet

– Income statement

– Statement of retained earnings

– Post-closing trial balance

The financial statements must be created in one Microsoft Word document (.doc or .docx file). Alternatively, an Excel workbook may be used (.xls or .xlsx file). The Word or Excel file will be uploaded for grading.The following financial statements are provided from the prior accounting period for J & L Accounting, Inc.:

a) Post-closing trial balance

b) Balance sheet

c) Income statement

d) Statement of retained earnings

J & L Accounting, Inc.

Post-Closing Trial Balance

December 31, 2014

BALANCE

ACCOUNT TITLE DEBIT CREDIT

Cash, Business Checking 20,500.00

Accounts Receivable –

Prepaid Rent –

Vehicles 48,000.00

Accumulated Depreciation, Vehicles 12,000.00

Equipment 3,600.00

Accumulated Depreciation, Equipment 600.00

Accounts Payable

Common Stock 38,000.00

Retained Earnings 21,500.00

Dividends

Service Revenue

Advertising Expense

Rent Expense

Office Supplies Expense

Telephone Expense

Utilities Expense

Depreciation Expense

TOTALS $72,100.00 $72,100.00

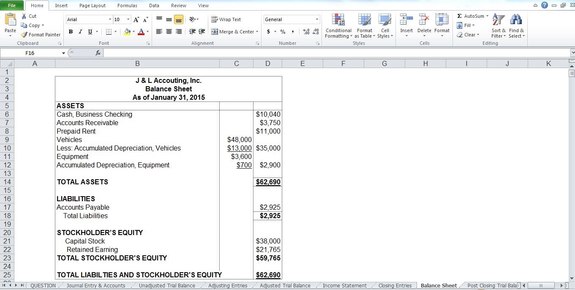

J & L Accounting, Inc.

Balance Sheet

As of December 31, 2014

ASSETS

Cash, Business Checking 20,500.00

Accounts Receivable –

Prepaid Rent –

Vehicles 48,000.00

Less: Accumulated Depreciation, Vehicles 12,000.00 36,000.00

Equipment 3,600.00

Less: Accumulated Depreciation, Equipment 600.00 3,000.00

TOTAL ASSETS $59,500.00

LIABILITIES

Accounts Payable –

TOTAL LIABILITIES –

STOCKHOLDERS’ EQUITY

Common Stock 38,000.00

Retained Earnings 21,500.00

TOTAL STOCKHOLDERS’ EQUITY 59,500.00

TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY $59,500.00

J & L Accounting, Inc.

Income Statement

For the Month Ending December 31, 2014

REVENUES

Service Revenue 10,275.00

EXPENSES

Advertising Expense 2,300.00

Rent Expense 1,000.00

Office Supplies Expense 300.00

Telephone Expense 750.00

Utilities Expense 3,200.00

Depreciation Expense 1,100.00

TOTAL EXPENSES 8,650.00

NET INCOME $1,625.00

J & L Accounting, Inc.

Statement of Retained Earnings

For the Month Ending December 31, 2014

Retained Earnings, December 1, 2014 19,875.00

Add: Net Income 1,625.00

Subtotal 21,500.00

Less: Dividends –

Retained Earnings, December 31, 2014 $21,500.00

1) Using the following blank forms (make as many copies as necessary), set up the general ledger accounts for the general ledger and insert the beginning balances for the accounts from the post-closing trial balance. The balances from the post-closing trial balance become the beginning balances of the accounts for the next account period.

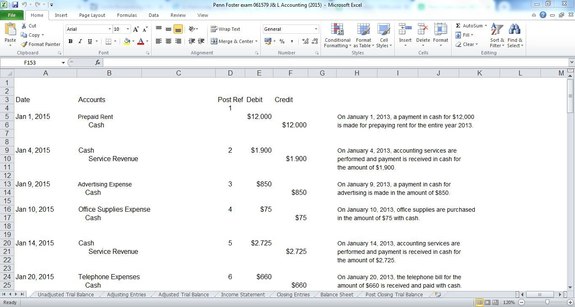

2) Journalize the following transactions in the general journal using the following blank form (make as many copies as needed). When making journal entries, each individual journal entry’s debits should equal its credits. (The amount for a journal entry can be incorrect or the entry can be incorrect. However, the debits still have to equal the credits even though the entry is incorrect. If the journal entry is incorrect, it can be corrected later when making adjusting/correcting journal entries. For example, if the amount is supposed to be $1,100, and for some reason the amount of $1,010 is recorded, this is acceptable—although incorrect, it can be corrected later.) The total of the debits must always equal the total of the credits for each journal entry—always. This is a fundamental GAAP that cannot be violated.

a. On January 1, 2015, a payment in cash for $12,000 is made for prepaying rent for the entire year 2013.

b. On January 4, 2015, accounting services are performed and payment is received in cash for the amount of $1,900.

c. On January 9, 2015, a payment in cash for advertising is made in the amount of $850.

d. On January 10, 2015, office supplies are purchased in the amount of $75 with cash.

e. On January 14, 2015, accounting services are performed and payment is received in cash for the amount of $2,725.

f. On January 20, 2015, the telephone bill for the amount of $660 is received and paid with cash.

g. On January 20, 2015, the utilities bill for $2,925 is received. The bill won’t be paid until it is due on

February 15, 2015.

h. On January 27, 2015, accounting services are performed on account in the amount of $3,750.

i. On January 28, 2015, a payment in cash for $1,500 is made for a bill from an advertising agency.

3) Post the general journal entries from the journal to the corresponding general ledger accounts, paying particular attention to the posting being made (debit or credit). Use the Post Ref. column to ensure that each line item of the journal entries is posted correctly to each general ledger account. Posting from the journal to the general ledger is nothing more than rearranging the information. If the

debits equal the credits for a particular journal entry and the information is posted correctly, the total of the debits should equal the total of the credits in the general ledger.

4) Calculate the balances in the general ledger accounts.(Use an Excel spreadsheet or a printing calculator, and run the numbers several times for accuracy. Often, debits won’t equal credits on the trial balance because a hand-held calculator is used and the math is done only once. Using a hand-held calculator can introduce errors.This is why an Excel spreadsheet is recommended. However,if a hand-held calculator is all that’s available to you, be sure to do the math enough times that you know the calculations are accurate.) To calculate the balances in the ledger accounts, you’ll need to do the following:

1) Add the debits.

2) Add the credits.

3) Subtract the larger amount from the other, or,alternatively, keep the running balance of the amount in the account and whether it’s a debit or credit on the ledger.

5) Create an unadjusted trial balance from the balances in the general ledger accounts. (Once again, be very careful when doing the math. When calculating the totals of the debit and credit columns, they should be equal. If not,do not continue until the debits equal the credits. An error has been made and must be found and corrected from the previous steps.) See page 129 of the text for an example of an unadjusted trial balance. Use the following blank form.

6) Journalize the following adjusting journal entries in the general journal, being sure that the debits equal the credits:

a. Calculate and make the adjustment for the amount of pre-paid rent that has been used.

b. Make an adjusting journal entry in the amount of $1,000 for depreciation of the vehicles.

c. Make an adjusting journal entry in the amount of $100 for depreciation of the equipment.

7) Post the adjusting journal entries to the respective general ledger accounts, again being sure that the postings are to the correct debit or credit side and that the Post Ref. column is used.

8) Calculate the new balances in the general ledger accounts.Create an adjusted trial balance from the balances in the general ledger accounts using the same blank form provided in step 5 when you created the unadjusted trial balance. See Exhibit 3-3 on page 114 in your textbook for an example of an adjusted trial balance. Make sure the math is correct and that the debit column is equal to the credit column. If not, don’t continue until the error has been found.

9) Create the income statement for J & L Accounting, Inc.using the information from the adjusted trial balance. Use the following blank form to create the income statement.Its format should be the same as the format used for the statement provided at the beginning of the project for the prior accounting period.

10) Create the closing journal entries in the general journal to close the revenue, expense, and dividend accounts to the retained earnings account, paying attention to debits equaling credits.

11) Post the closing journal entries to the respective generalledger accounts.

12) Calculate the balances in the general ledger accounts.

13) Create a post-closing trial balance from the balances in the general ledger accounts using the same blank form that was provided in step 5 when you created the unadjusted trial balance. The post-closing trial balance should be in the same format as the post-closing trial balance provided at the beginning of the project for the prior accounting period. Make sure the math is correct and that the debit column is equal to the credit column.If not, don’t continue until the error has been found.

14) Create the balance sheet for J & L Accounting, Inc. using the information from the post-closing trial balance. If the debits equal the credits from the previous work and the closing entries were made properly, then the accounting equation should balance on the balance sheet. If the assets don’t equal the liabilities plus stockholders’ equity, an error has been made that needs to be corrected. The balance of the accounting equation is another fundamental GAAP principle that can’t be violated. Use the following form to create the balance sheet. Its format should be the same as the format of the statement provided at the beginning of the project for the prior accounting period.

15) Create the statement of retained earnings for J & L Accounting, Inc. using the ending balance from the statement of retained earnings from the prior period and the net income from the income statement for the January accounting period. (No dividends were paid out during the month of January.) Follow the same format from the statement of retained earnings at the beginning of the graded project for the prior accounting period using the blank form on the following page.

ciciliany

ciciliany