Ice Cream Systems

The goal of this graded project is to create the following financial statements for Ice Cream Systems (ICS):

Balance sheet

Income statement

Post-closing trial balance

Note: It's important to format financial statements properly. They must follow Generally Accepted Accounting Principles (GAAP), which create a uniformity of financial statements for analyzing. This allows for an easier comparison, as all businesses follow GAAP. Therefore, the financial statements you create should replicate those in the textbook.

This project references "debits equaling credits." This is a fundamental principle of accounting, and violation of this principle is not acceptable under any circumstance. If debits don't equal credits, it suggests that someone has "cooked the books" or presented false information. It also allows for

embezzlement. If debits don't equal credits, the cause may be a lack of understanding of accounting principles or carelessness when making journal entries, posting to the general ledger accounts, or completing the math. Remember that instructors are available to help you! If your mistakes are careless, go back over the work slowly until the error is found.

The accounting equation must balance on the balance sheet. This is another fundamental principle of accounting that can't be violated. Unbalanced equations are completely unacceptable. When the equation doesn't balance, it's easily detectable by someone who knows accounting, and it suggests the numbers have been "fudged." If your debits equal your credits and you understand which general ledger accounts belong on which financial statements, then the accounting equation should balance. It's really all about understanding the concepts and applying that understanding.

The following financial statements are provided for ICS:

Chart of Accounts

Post-Closing Trial Balance

Schedule of Accounts Receivable

Schedule of Accounts Payable

Schedule of Employer Payroll Taxes Allocation

Format for the Income Statement

Format for the Balance Sheet

Job Cost Record

Chart of Accounts

Assets (1000-1999)

Account Number

Account Title

1100

Cash

1200

Accounts Receivable

1300

Direct Materials

1350

Indirect Materials and Factory Supplies

1400

Work in Process

1500

Finished Goods

1600

Prepaid Advertising

1650

Prepaid Insurance

1700

Office Supplies

1800

Factory Equipment

1800.1

Accumulated Depreciation—Factory Equipment

1850

Office Equipment

1850.1

Accumulated Depreciation—Office Equipment

Liabilities (2000-2999)

2100

Accounts Payable

2200

Salaries Payable

2300

Federal Withholding Tax (FWT) Payable

2325

FICA Tax Payable

2350

FUTA Tax Payable

2375

SUTA Tax Payable

2500

Unearned Revenue

(Continued)

Owner's Equity (3000-3999)

3100

Common Stock ($10 Par)

3150

Paid-In Capital in Excess of Par—Common Stock

3700

Retained Earnings

3900

Income Summary

Revenues (4000-4999)

4100

Sales

4200

Sales Discounts

Expenses (5000-5999)

5100

Cost of Goods Sold

5150

Factory Overhead

5200

Sales Salaries Expense

5225

Officers' Salaries Expense

5250

Office Salaries Expense

5300

Rent Expense

5350

Advertising Expense

5400

Utilities Expense

5450

Office Supplies Expense

5500

Postage Expense

5550

Telephone Expense

5575

Insurance Expense

5600

Depreciation Expense

5700

Payroll Tax Expense

5800

Bad Debt Expense

5900

Miscellaneous Expense

ICE CREAM SYSTEMS

Trial Balance January 1, 20—

ACCOUNT NO.

DESCRIPTION

DEBIT

CREDIT

1100

Cash

$117,964.23

1200

Accounts Receivable

51,484.00

1300

1350

Direct Materials

Indirect Materials &

64,350.00

18,772.00

1400

Factory Supplies

Work in Process

142,695.00

1500

Finished Goods

27,696.00

1600

Prepaid Advertising

—

1650

Prepaid Insurance

—

1700

Office Supplies

342.25

1800

Factory Equipment

246,857.00

1800.1

Accumulated Depreciation—

Factory Equipment 99,653.35

1850 Office Equipment 38,567.00

1850.1 Accumulated Depreciation—

2100

Office Equipment

Accounts Payable

9,814.00

2200

Salaries Payable

—

2300

FWT Payable

1,613.11

2325

FICA Tax Payable

822.68

2350

FUTA Tax Payable

1,032.39

2375

SUTA Tax Payable

1,871.20

2500

Unearned Revenue

—

3100

Common Stock ($10 Par)

350,000.00

18,845.66

3150

Paid-In Capital in Excess of

Par—Common 32,500.00

3700 Retained Earnings 192,575.09

TOTALS $708,727.48 $708,727.48

ICE CREAM SYSTEMS

Schedule of Accounts Receivable

January 1, 20—

Name

Balance

Horsfield Happy Ice Cream

$17,345.00

Messina Missions

9,458.00

Ashman Alcove Designs

24,681.00

Day Dreamer's Ice Cream

0.00

Total Accounts Receivable

$51,484.00

ICE CREAM SYSTEMS

Schedule of Accounts Payable

January 1, 20—

Name

Balance

O-Ring Enterprises

$6,941.00

Smith Synthetics

0.00

Rockaway Metal

2,873.00

OfficeMax

0.00

Total Accounts Payable

$9,814.00

ICE CREAM SYSTEMS

Schedule of Employer Payroll Tax Allocation

January 31, 20—

Employer Payroll Taxes

Job

Wages

FWT (15%)

FICA (7.65%)

FUTA (0.8%)

SUTA (1.45%)

Total Employer Taxes

Net Pay

Direct Labor Totals

Sales Salaries

Officers' Salaries

Office Salaries

Totals

EXAMPLE COMPANY

Income Statement

For the Period Ending January 31, 20XX

Operating Revenue

Sales

Less: Sales Discounts

$ XXXXX.XX

XXX.XX

Total Operating Revenue

Cost

$ XXXXX.XX

COGS—Cost of Goods Sold

XXXXX.XX

Total Cost

XXXXX.XX

Gross Profit

XXXXX.XX

Operating Expenses

Sales Salaries Expense

XXXXX.XX

Officers' Salaries Expense

XXXXX.XX

Office Salaries Expense

XXXXX.XX

Rent Expense

XXXXX.XX

Advertising Expense

XXXXX.XX

Utilities Expense

XXXXX.XX

Office Supplies Expense

XXXXX.XX

Postage Expense

XXXXX.XX

Telephone Expense

XXXXX.XX

Insurance Expense

XXXXX.XX

Depreciation Expense

XXXXX.XX

Payroll Tax Expense

XXXXX.XX

Bad Debt Expense

XXXXX.XX

Miscellaneous Expense

XXXXX.XX

Total Operating Expenses

XXXXX.XX

Net Profit/(Loss)

$XXXXX.XX

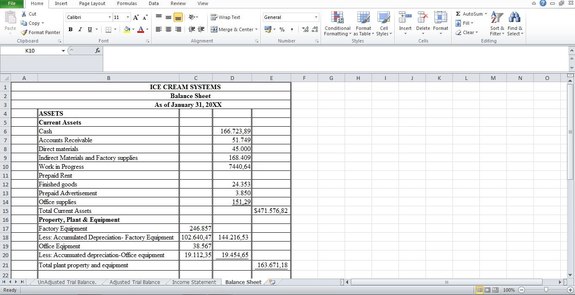

EXAMPLE COMPANY

Balance Sheet

As of January 31, 20—

ASSETS

Current Assets

Cash

$XXXXX.XX

Accounts Receivable

XXXX.XX

Direct Materials

XXXX.XX

Indirect Materials and Factory Supplies

XXXX.XX

Work In Process

XXXX.XX

Finished Goods

XXXX.XX

Prepaid Advertising

XXXX.XX

Prepaid Insurance

XXXX.XX

Office Supplies

XXXX.XX

Total Current Assets

$XXXXX.XX

Property, Plant & Equipment

Factory Equipment

$XXXXX.XX

Less: Accumulated Depreciation— Factory Equipment

XXXXX.XX

XXXXX.XX

Office Equipment

XXXX.XX

Less Accumulated Depreciation— Office Equipment

XXXX.XX

XXXX.XX

Total Property Plant & Equipment

XXXXX.XX

TOTAL ASSETS

$XXXXX.XX

LIABILITIES

Accounts Payable

$XXXX.XX

Salaries Payable

XXXX.XX

FWT Payable

XXXX.XX

FICA Tax Payable

XXXX.XX

FUTA Tax Payable

XXXX.XX

SUTA Tax Payable

XXXX.XX

Unearned Revenue

XXXX.XX

TOTAL LIABILITIES

$XXXXX.XX

STOCKHOLDERS' EQUITY

Common Stock ($10 Par)

$XXXXXX.XX

Paid-In Capital in Excess of Par—Common Stock

XXXXXX.XX

Retained Earnings

XXXXXX.XX

TOTAL STOCKHOLDERS' EQUITY

XXXXXX.XX

TOTAL LIABILITIES AND STOCKHOLDERS' EQUITY

$XXXXXX.XX

The following is the background information necessary for completion of the accounting period as it relates to Ice Cream Systems Inc. (ICS):

ICS manufactures and sells ice cream machines, refrigeration systems, and parts for these systems. It manufactures all machines and parts in a single production department.

As the controller of the company, you are responsible for daily accounting operations, adjusting and closing the monthly accounting periods, and preparation of financial statements.

ICS operates on a calendar-year basis from January 1st to December 31st with a monthly accounting period. It uses a job-order cost system.

Jobs that are in process are recorded on Job Cost Records. Records are maintained for each job. New jobs are assigned numbers sequentially. They contain the accumulated costs for direct material, direct labor, and factory overhead. (For the purposes of this project, it's assumed that all jobs prior to the current accounting period are either in process or complete and all resulting entries have been made in the previous accounting period.)

ICS makes all journal entries in the General Journal. No special journals are used.

For purposes of this project, cash doesn't need to be rec- onciled to a bank statement.

Information related to Payroll:

Payroll is paid monthly on the last day of each month. Therefore, there is no accrual for payroll.

Gross pay for direct labor goes to Finished Goods or Work in Process if appropriate.

Salaries for non-factory workers go to the appropriate salary expense accounts.

The company's salesperson works on 10% straight commission of sales during the month.

Federal Withholding Tax is 15% of gross pay for everyone and is recorded whenever gross pay is recorded. FWT is remitted monthly for the previous month.

There are no deductions for state or local withholding tax.

FICA tax rate is 7.65% of gross pay. (FICA is Social Security and Medicare.) Since this is the first month of the new year, no one will reach the Social Security limit. FICA is remitted monthly for the previous month.

FUTA tax rate is 0.8% of gross wages with no limit. SUTA tax rate is 1.45% of gross wages with no limit. FUTA and SUTA are paid yearly in January (for the previous year).

There are no other miscellaneous deductions, such as union dues.

All employer payroll taxes (employer's portion of FICA, FUTA, and SUTA) are recorded on the last day of the month.

Employer payroll taxes related to factory workers go to Factory Overhead.

Employer payroll taxes related to all non-factory workers go to Payroll Tax Expense.

ICS has two material accounts:

Direct Materials

Indirect Materials and Factory Supplies

Factory Overhead is applied to each job at 25% of direct labor costs for that job.

Debits to Factory Overhead represent actual overhead, and credits represent applied overhead. The difference between actual and applied factory overhead is insignifi- cant and should be closed out to Cost of Goods Sold as an adjusting entry at the end of each month.

Markups to determine the selling price of a job for ICS are 150% of estimated job costs. All sales are exempt from sales tax, as ICS sells locally to resellers.

Shipping is not a consideration for the purposes of this project.

ICS uses a perpetual inventory system. When a sale is made, debit Cost of Goods Sold and credit Finished Goods for the cost of the job.

All sales are on account with terms of net 30 days. No discounts are given.

All cash/checks received are deposited in the Cash account.

No separate bank account is kept for payroll.

Direct materials, indirect materials, and factory supplies are purchased on account.

Terms from all vendors for expenses are net 30 days.

Factory Supplies are added to the Indirect Materials and Factory Supplies general ledger account.

A periodic inventory system is used for office supplies with all purchases going to inventory.

All payments—referred to as cash or check—are made by check from the Cash Account. (For purposes of this project, no check register or checks will be given. No reconciliation of the cash account will be required. Assume that all checks are written.

Set up the General Ledger accounts, Accounts Receivable, and Accounts Payable accounts. Use the following blank forms (make as many copies as necessary). Insert the beginning balances from the Trial Balance and Schedules of Accounts Receivable and Payable.

1. Journalize the following entries for the month of January in the General Journal. Use the following blank forms (make as many copies as necessary). When using the Work in Process account, be sure to post to the appropriate Job Cost Record.

Narrative of Transactions

January 2—Paid Mass Media $4,200.00 for prepaid advertising in local newspapers for the next 12 months.

January 2—Paid Pierce Properties $2,750.00 for January rent. Of this amount, 25% is for office facilities and 75% is for factory facilities.

January 2—Paid Owen's Insurance $6,000.00 for prepaid insurance for the first quarter of the year.

January 3—Received a check from Horsfield Happy Ice Cream as partial payment on account in the amount of $5,000.00.

January 3—Paid Rockaway Metal the balance of $2,873.00 on account.

January 4—Sold two ice cream systems to Day Dreamer's Ice Cream. The estimated direct labor is

$8,200.00. The estimated direct material is $3,350.00. The estimated indirect material is $350.00. Day Dreamer's is to be billed in the amount of $20,925.00 on account. A check for $5,000.00 will be collected as a deposit against that sale. The start date will be January 7th. The date promised will be January 23rd. Assign the contract to Job 74.

January 5—Mountain Swirl Ice Cream purchased and took delivery of one ice cream machine for

$7,500.00. Record the sale and the cost of the sale. Markup is 150% of cost. Transfer cost from Finished Goods to COGS.

January 6—Purchased indirect material on account from Electrical Systems Corp. in the amount of

$3,643.00. Set up a new Accounts Payable account, and record the purchase.

January 6—Purchased factory supplies on account from Grommet Supplies in the amount of

$847.21. Set up a new Accounts Payable account, and record the purchase.

January 9—Assign the manufacture of one ice cream machine to Job 75. A direct material requisi- tion shows $1,450.00 of direct materials, and an indirect materials requisition shows $170.00 of indirect materials. A time card shows $3,650.00 of direct labor for the completed job. Factory overhead is based on 25% of direct labor cost. Transfer the completed job from Direct Material and Indirect Material to the Finished Goods account. When making the journal entry for applying direct labor, debit Finished Goods for the gross pay and credit FWT Payable and FICA Tax Payable for the appropriate amounts with the net pay going to Salaries Payable.

January 10—Receive a check from Horsfield Happy Ice Cream as partial payment on account in the amount of $5,000.00.

January 10—Receive a phone bill in the amount of $1,402.22 from Unique Telephone Systems on account.

January 15—Paid Liberty Bank $2,435.79 for December payroll taxes payable for the amounts of FWT Payable, $1,613.11; FICA Tax Payable, $822.68.

January 15—Assign Job 76 to Cold Refrigeration for the purchase of a refrigeration system. The start date will be January 16th. The completion date will be no later than February 28th. The esti- mated direct material is $9,175.00. The estimated indirect material is $1,860.00. The estimated direct labor is $15,600.00. The contract amount is $45,800.00. A deposit of $10,000.00 was pro- vided by Cold Refrigeration in signing the contract. The deposit is unearned revenue. Half of the contract will be billed upon 50% completion with the deposit applied against that billing with the remaining amount due immediately. A quarter of the contract will be billed upon 75% completion of the contract with the amount due immediately. The remaining amount of the contract is to be billed when the job is 100% complete and is payable within 30 days of the billing.

January 16—Purchased $4,441.00 of factory supplies from Johnston Equipment paid in cash.

January 16—Purchased $2,965.00 of direct materials from Smith Synthetics on account.

January 16—Purchased $427.50 of office supplies from OfficeMax on account.

January 19—Apply from direct materials requisition $2,800.00 of direct materials. Apply from indi- rect materials requisition $325.00 of indirect materials. Apply from time cards $7,950.00 of direct labor to Job 74 completing the job. Applied factory overhead is based on 25% of direct labor cost. Transfer the completed job to the COGS account from Direct Material and Indirect Material and Factory Overhead accounts. When making the journal entry for applying direct labor, debit COGS for the gross pay and credit FWT Payable and FICA Tax Payable for the appropriate amounts with the net pay going to Salaries Payable.

January 20. —Paid the electric bill from Susquehanna Electric in the amount of $2,356.21 for the month of December. Allocate 30% to Factory Overhead.

January 20—Paid the FUTA Tax Payable for the previous year.

January 20—Paid the SUTA Tax Payable for the previous year.

January 23—Ashman Alcove Designs paid the balance on account.

January 27—Paid O-Ring Enterprises the balance owed on account.

January 27—Paid post office $300.00 cash for postage added to postage meter.

January 28—Apply from direct materials requisition $4,600.00 of direct materials. Apply from indirect materials requisition $950.00 of indirect materials. Apply $8,000.00 (from time cards) of direct labor and factory overhead to Job 76, completing 50% of the job. Factory overhead is based on 25% of direct labor cost. Transfer the partially completed job from Direct Material and Indirect Material to WIP. When making the journal entry for applying direct labor, debit WIP for the gross pay and credit FWT Payable and FICA Tax Payable for the appropriate amounts with the net pay going to Salaries Payable. Set up the accounts receivable and bill Cold Refrigeration for 50% of the contract on account, applying the initial $10,000.00 deposit against the billing.

January 29—Received a check from Cold Refrigeration in the amount of $9,976.25 on account.

January 31—Received the following data for the monthly payroll: Direct labor (already recorded) $19,600.00 Sales commission 5,132.50

Officers' salaries 5,000.00

Office salaries 1,920.00

Record the monthly payroll. Direct labor payroll has already been recorded, as it was incurred in January. Debit other salary expense accounts for the appropriate amounts; credit FWT Payable

for 15% of gross pay; credit FICA Tax Payable for 7.65% of gross pay; and credit Salaries Payable for the net pay. Record the payroll taxes imposed on the employer for all personnel for the month of January. (Prepare the "Schedule of Employer Payroll Taxes Allocation" using the appropriate

tax rates.)

January 31—Received a check from Messina Missions for the balance on account.

January 31—Received a check from Horsfield Happy Ice Cream for the remaining balance on account.

January 31—Paid all employee wages earned in January.

Post the general journal entries to the General Ledger, the Accounts Receivable Ledger, and the Accounts Payable Ledger. Use the Post Ref. column to ensure that each line item of the journal entries is posted correctly to each general ledger account. Posting from the journal to the ledger is nothing more than rearranging the information; however, focus and concentrate because it's easy to make a mistake.

Calculate the balances in the general ledger accounts. Use an Excel spreadsheet or a printing calculator to run the numbers several times. Don't use a hand-held calculator, as it's far too easy to make a mistake using it.

Prepare the Schedules of Accounts Receivable and Accounts Payable.

Prepare an Unadjusted Trial Balance using the balances from the general ledger accounts.

Journalize the following adjusting entries in the general journal.

Adjusting Entries

January 31—Expense Prepaid Advertising for the month of January.

January 31—Expense Prepaid Insurance for the month of January.

January 31—Office supplies physical inventory as of January 31 is $276.21.

January 31—Depreciation for the month of January for Factory Equipment is $2,987.12. Depreciation for Office Equipment is $266.99.

January 31—Close out Factory Overhead of $190.24 to Cost of Goods Sold.

Post the adjusting journal entries to their respective ledger accounts, and calculate new balances for those accounts.

Prepare an Adjusted Trial Balance using the balances from the general ledger accounts. Use the blank form provided in step six.

Prepare an Income Statement following the formats shown in the Example Company Statements using the following blank form as a worksheet:

Journalize and post the closing journal entries in the general journal.

Jan. 31—Prepare closing entries to close revenue and expense accounts to Income Summary, and transfer the net income to Retained Earnings.

Post the closing journal entries to the respective ledger accounts, and calculate new balances for those accounts.

Prepare a Post-Closing Trial Balance using the balances from the general ledger accounts. Use the blank form that was provided in step six.

From the Post-Closing Trial Balance, create the Balance Sheet following the formats shown in the Example Company Statements using the following blank form as a worksheet

ciciliany

ciciliany